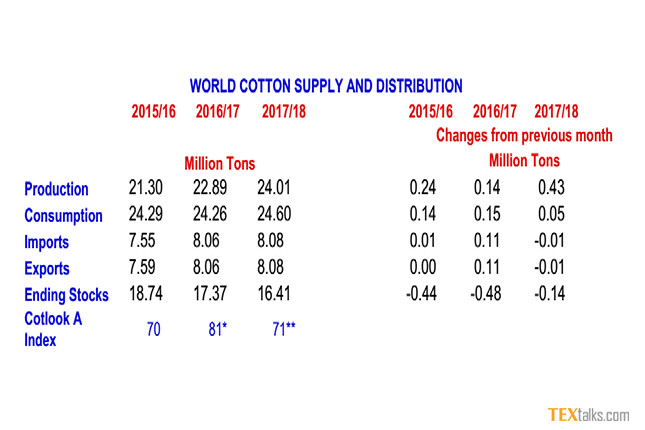

In 2016/17, world cotton production is estimated at 22.9 million tons while world mill use is projected at 24.3 million tons, which represents the second consecutive season where mill use has exceeded production. As a result, world ending stocks are forecast to decrease by 7% to 17.3 million tons. However, this decline occurs entirely within China where stocks at the end of July 2017 are projected down 17% to 9.2 million tons. Stocks held outside of China, however, are forecast to rise by 6% to 8 million tons. Despite the growth in stocks held outside of China, international cotton prices as measured by the Cotlook A Index have averaged 82 cts/lb from August 2016 through May 2017, which is well above the long-term average of 70 cts/lb.

Sales from China’s reserve through May 2017 reached over 1.1 million tons, which brings the total volume of cotton held by the Chinese government to 7.2 million tons. China’s cotton production declined by 2% to 4.9 million tons in 2016/17, but its mill use is projected to increase by 2% to 7.7 million tons. Imports by China are anticipated to increase by 10% to 1.06 million tons, which is the first increase since 2011/12, though any further increase is limited by the import quota. Thus, sales from the reserve are being used to make up for the shortfall in production while mill use is forecast to remain unchanged at 7.7 million tons in 2017/18.

Production outside of China is estimated up by 10% to 18 million tons in 2016/17 and is expected to grow by 5% to 19 million tons in 2017/18 due to the high prices prevailing this season. Cotton area in India is forecast to expand by 7% to 11.3 million hectares, and assuming yield is similar to the 4-year average of 528 kg/ha, production could increase by 3% to 6 million tons in 2017/18. Farmers in the United States are projected to expand cotton area to 4.6 million hectares with production expected to rise by 12% to 4.2 million tons. Pakistan’s cotton production is projected to increase by 13, and if high prices continue through the end of 2017, cotton production in Brazil could increase to 1.5 million tons. In 2017/18, world trade is expected to remain unchanged from 2016/17 at 8.1 million tons. Given that cotton production is projected to grow in the large consuming countries the need to import cotton will likely decrease.

After falling by 1% to 16.5 million tons in 2016/17, mill use outside of China may increase by 2% to 16.9 million tons in 2017/18 due to much stronger growth in the global economy in 2017 and 2018. Consumption in India is forecast to increase by 3% to 5.2 million tons in 2017/18 as prices for cotton and yarn are likely to be competitive due to the increase in supply. Pakistan’s mill use is expected to rise modestly by 1% to 2.3 million tons as competition from other mills in Asia remains stiff. Consumption in Bangladesh is projected to rise by 5% to 1.5 million tons while Turkey’s mill use is expected to decline by 15,000 tons to 1.4 million tons due to completion from other countries and weak domestic demand.