According to the report, global cotton production for the 2025/26 season is estimated at 26.5 million tonnes, up 3% from the previous season, while consumption is projected to reach 25.3 million tonnes, an increase of 1.6%. Looking ahead to 2026/27, global production is forecast to decline slightly by 2% to 25.9 million tonnes, while consumption is expected to continue growing, rising approximately 1% to 25.5 million tonnes. Global cotton trade is projected to increase by 2.6% to 9.6 million tonnes.

The report identifies several key trends shaping the market:

- Improving global demand for cotton consumption despite tighter production prospects.

- Continued pressure on cotton acreage as growers respond to weaker profitability, rising production costs, and competition from alternative crops.

- Climate-related challenges, including heat, unreliable rainfall, and increasing pest pressures, which continue to affect production decisions.

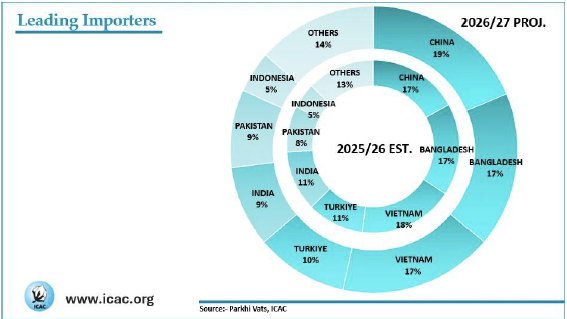

- A significant shift in global import demand, led by India and a recovering Chinese market.

India Emerges as a Major Demand Center

India has become one of the most important drivers of global cotton demand. Cotton lint imports are projected to reach approximately 1 million tonnes in the 2025/26 season, a 42% increase over the previous season and the highest level ever recorded by the country.

The surge follows a series of policy changes, including temporary reductions in import duties and exemptions for extra-long staple cotton, which improved access to imported fiber and supported domestic consumption growth.

China’s Cotton Imports Recover

China is expected to regain its position as the world’s largest cotton importer during the 2026/27 season, accounting for an estimated 19% of global imports.

Following an eight-year low in imports during the previous season, China’s cotton lint imports are projected to increase by approximately 42% in 2025/26, supported by additional import quotas, higher domestic cotton prices, and the need to sustain consumption levels.

Changing Trade Relationships

Brazil has consolidated its position as China’s largest cotton supplier, accounting for approximately 52% of China’s cotton imports during the current season. Australia has emerged as China’s second-largest supplier, while U.S.-China trade policies continue to influence global cotton trade flows and competitiveness.

The report also examines the implications of recent policy developments, including China’s suspension of tariffs introduced since March 2025 and new commitments to purchase U.S. agricultural products.

US Cotton Policy Initiatives

The July issue highlights the launch of the Great American Cotton Plan by the U.S. Department of Agriculture. The initiative aims to increase domestic demand for American-grown cotton and cotton products, strengthen the cotton value chain, and improve returns for growers.

The plan includes the “Plant Not Plastic” initiative, which promotes cotton-based products as sustainable alternatives to synthetic fibers, as well as support for the proposed Buying American Cotton Act.

ICAC’s Price Projections

Based on current supply and demand projections, the Secretariat forecasts the Cotlook A Index for the 2026/27 season to range between 66 and 85 cents per pound, with a midpoint of 75.7 cents per pound.

ICAC’s Statistical Data Portal

Consult ICAC’s Statistical Data Portal, which is updated continuously throughout the month.

The author of Cotton This Month is Parkhl Vats, Principal Statistician & Data Architect at ICAC.

The next issue of Cotton This Month will be released on August 1, 2026.